US Dollar and Rates Pullback After Core Inflation Beats Expectations

January 15, 2025

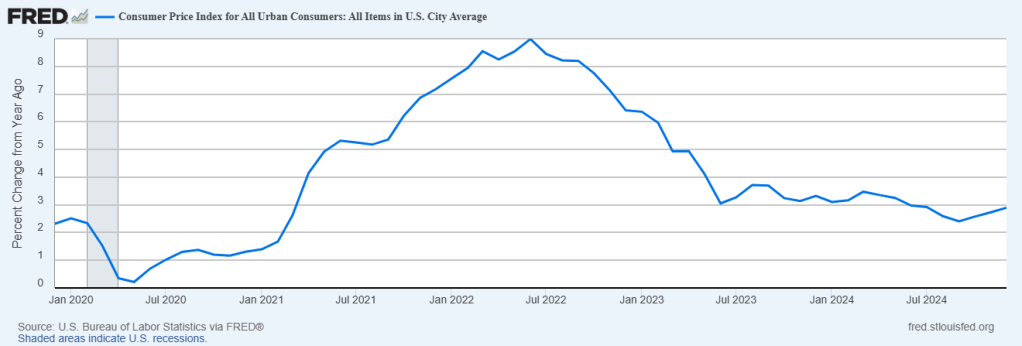

Consumer Price Index (CPI)

inflation increased by 0.4% in December, which was right in line with expectations. Headline inflation was most affected by the volatile energy category, which increased 2.6% for the month.

CPI

is up 2.9% over the last 12 months; up from a 2.7% increase over the 12 months ending in November. It’s the 3rd straight annualized increase in the CPI.

Core CPI

(which excludes the volatile food & energy prices) increased 0.2% in December, which was better than the 0.3% that the market was anticipating.

Core inflation is up 3.2% from last year, but that is the slowest rate of price increases in 3.5 years.

Breaking down the monthly price increases by category, all but one category (medical care commodities) was higher, with energy being the biggest driver of inflation for December.

On an annualized basis, 7 of 10 consumer categories are higher than a year ago. Transportation, shelter, and services inflation lead the way, while energy and vehicles are the laggards.

In response to the data, the

US Dollar

is down about 0.5% this morning. What would be the 3rd straight down day after hitting resistance around $110?

Rates are also falling after the data release. The

United States 10-Year

is back below the 2024 high point. A welcome outcome for equities. The combo of falling USD and rates are easing financial conditions. At least for now.

As a result, the market is up over 1.5% so far. Looks like a retest of the downtrend line is in the cards; although the midpoint of this current pullback (red line) and the 50-day moving average (white) still stand in the way.

Inflation was a little better than anticipated, but this was by no means a big win. Headline inflation still increased at a higher rate than in the last few months, and core inflation is still over 50% above the Fed’s price stability mandate.

Core CPI

(which excludes the volatile food & energy prices) increased 0.2% in December, which was better than the 0.3% that the market was anticipating.

Core CPI

(which excludes the volatile food & energy prices) increased 0.2% in December, which was better than the 0.3% that the market was anticipating.